IFAC_Definition_of_MA.jpg

No higher resolution available.

Summary

| Description |

English:

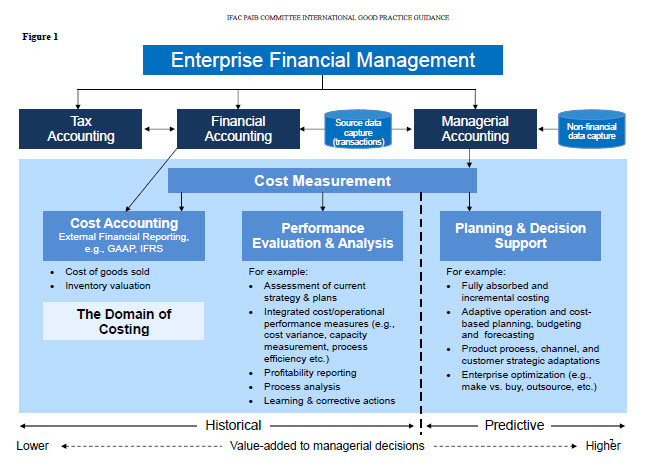

Published in the International Good Practice Guidance: Evaluation and Improving Costing in Organizations July 2009

|

| Date | |

| Source | International Federation of Accountants |

| Author | Professional Accountants in Business Committee |

|

This

diagram

image could be re-created

using

vector graphics

as an

SVG

file

. This has several advantages; see

Commons:Media for cleanup

for more information. If an SVG form of this image is available, please upload it and afterwards replace this template with

{{

vector version available

|

new image name

}}

.

It is recommended to name the SVG file “IFAC Definition of MA.svg”—then the template Vector version available (or Vva ) does not need the new image name parameter. |

Licensing

|

The copyright holder of this file allows anyone to use it for any purpose, provided that the copyright holder is properly attributed. Redistribution, derivative work, commercial use, and all other use is permitted. |

|

|