Pareto_Efficient_Frontier_for_the_Markowitz_Portfolio_selection_problem..png

Size of this preview:

800 × 538 pixels

.

Other resolutions:

320 × 215 pixels

|

640 × 430 pixels

|

1,024 × 689 pixels

|

1,392 × 936 pixels

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

|

This

graph

image could be re-created

using

vector graphics

as an

SVG

file

. This has several advantages; see

Commons:Media for cleanup

for more information. If an SVG form of this image is available, please upload it and afterwards replace this template with

{{

vector version available

|

new image name

}}

.

It is recommended to name the SVG file “Pareto Efficient Frontier for the Markowitz Portfolio selection problem..svg”—then the template Vector version available (or Vva ) does not need the new image name parameter. |

Summary

| Description |

English:

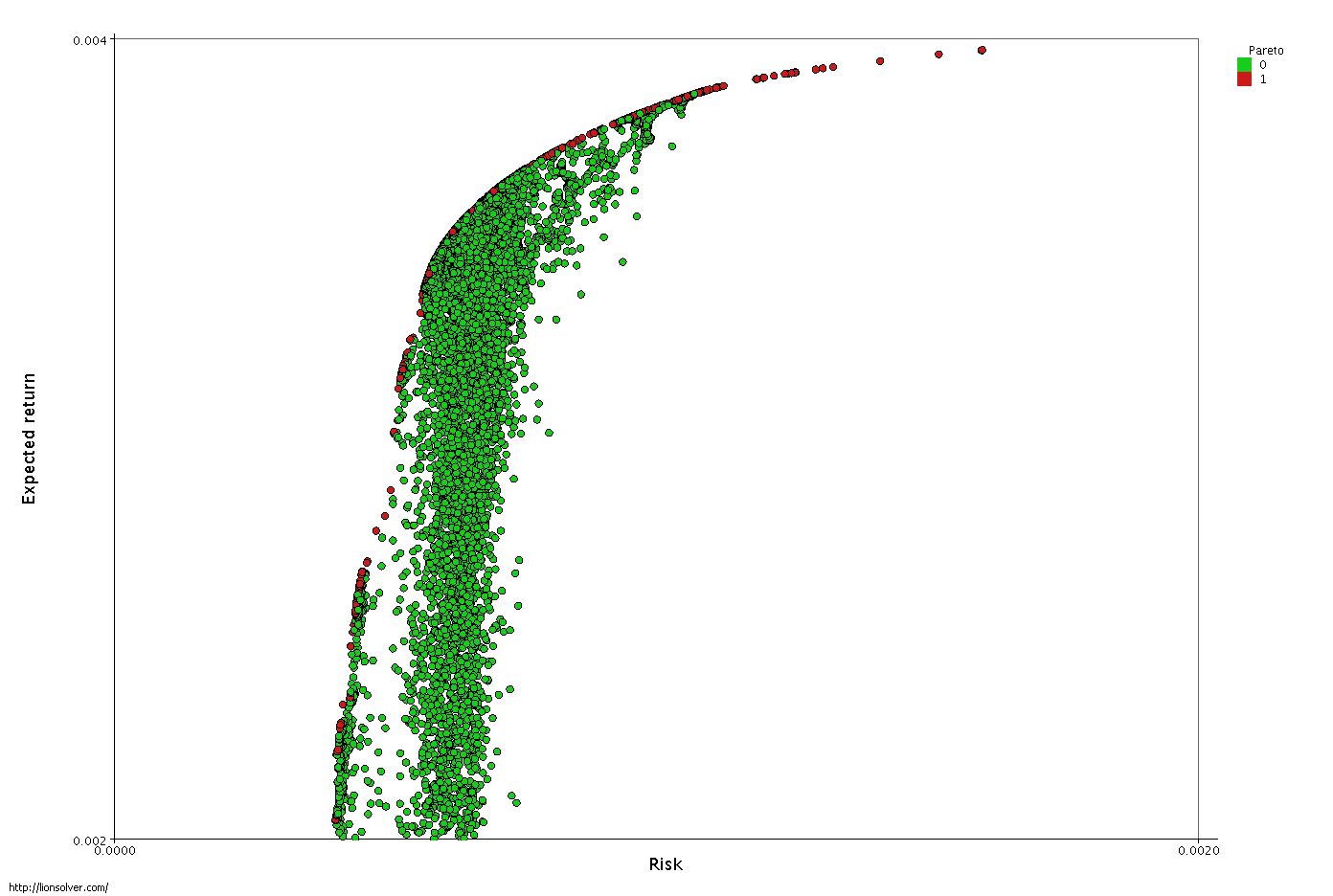

The problem consists of selecting a set of assets and choosing the share of investment dedicated to each asset, in order to follow the investor's desires regarding return and risk.

The classic and seminal approach to this problem is due to Markowitz (1952). The plot shows the results of optimizing 225 stocks by using the LIONsolver software, Pareto-optimal solutions are red. ( created with

http://LIONsolver.com

)

|

| Date | |

| Source | Own work |

| Author | Marcuswikipedian |

Licensing

I, the copyright holder of this work, hereby publish it under the following license:

This file is licensed under the

Creative Commons

Attribution-Share Alike 3.0 Unported

license.

-

You are free:

- to share – to copy, distribute and transmit the work

- to remix – to adapt the work

-

Under the following conditions:

- attribution – You must give appropriate credit, provide a link to the license, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use.

- share alike – If you remix, transform, or build upon the material, you must distribute your contributions under the same or compatible license as the original.